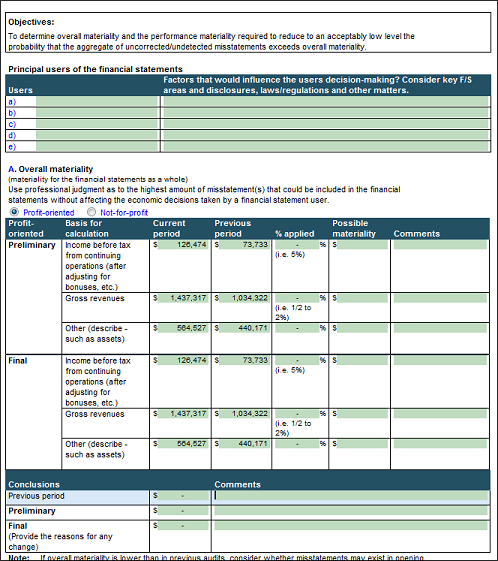

Materiality

Materiality (CORE) documents (420. and 420C.) allow you to determine materiality for the engagement. Condensed audit form 420C. is intended for use on smaller engagements by auditors who understand the ISA requirements. Materiality is set for each engagement for:

-

Overall Materiality - based on the auditor's professional judgment as to the highest amount of misstatement that could be included in the financial statements without affecting the economic decisions taken by a financial statement user. Overall materiality flows through to the Financial Statement Areas worksheet (FSA), which is used to flag material financial statement areas.

-

Performance Materiality - performance materiality is set at a lower amount than overall materiality. It provides a margin or buffer so that individually immaterial misstatements will not accumulate to an amount that would materially misstate the financial statements. Performance materiality flows through to the Financial Statement Areas worksheet (FSA), which is used to flag material financial statement areas.

-

Specific materiality - in some cases, there may be a need to provide a larger buffer or to identify misstatements or events that are much smaller than would be identified by using performance materiality at the financial statement level. Specific materiality relates to classes of transactions, account balances, disclosures or other considerations.

-

Trivial materiality - in some cases, there may be a need to provide an amount below which misstatements would be clearly trivial. Whether taken individually or in aggregate, such amounts clearly would not have a material effect on the financial statements.

Materiality assists in identifying significant areas in the financial statement areas worksheet. Should the preliminary assessment of materiality and audit risk change from initial planning to the time of evaluating the results of the audit, the audit response and procedures should be updated accordingly.

The materiality document also allows for the manual input of values. Additionally, menu items and right-click functionality exists within the document to add, delete, and sort rows.