Consolidation Methods

Select the way you want the data from the subsidiaries and divisions to be consolidated into the parent company. There are three ways to consolidate files in Working Papers:

Real-time consolidation (internal)

Consolidation can be done within a file at multiple levels and updated in real-time. Although the process of combining subsidiary client files that are maintained separately from the consolidated file can still be used, many situations exist where it is far more practical and efficient to combine and consolidate accounts for different types of entities in one file.

| Advantages | Disadvantages |

|---|---|

| -allows entry of general ledger detail | -the user must sign out/check out to work on an entity (copies whole file) |

| -facilitates monthly and quarterly statements since all other entry details are maintained | -for very large internal consolidation files, there is a greater risk of running into the general limitation of 2GB for any of the files that make up the client file (e.g. .dbf, .fpt, .cdx) |

| -only one file needs to be maintained | -where sub entities require their own separate work papers (i.e. separate engagements), the document manager of the internal consolidated file can become unwieldy |

Batch consolidation (external)

Working Papers creates a link from the consolidated file to client files maintained externally. This is useful if records for the combined entities are entered and updated on different computers or networks. Once the individual client files are completed, the entities are consolidated into one file.

| Advantages | Disadvantages |

|---|---|

| -facilitates remote use of individual entities by allowing users to work on an entity out in the field or different location | -many client files need to be maintained and kept track of |

|

-audit planning process and working papers: →audit plans and documentation for a group of related entities can be

placed in a single consolidated file |

-sign out may require the user to reconnect the file paths to all of the external files |

| -easier to maintain if separate reporting is required for each entity | -detailed general ledger transactions are not maintained in the consolidated file; they can only be viewed from the external client file |

Combining batch files and real-time files

Should circumstance require, you can combine and consolidate a file that is a mixture of both real-time and batch files. However, it may be easier to maintain and track if only one method is used.

If a combined approach is used, converting an external entity into an internal entity should be avoided.

For example, when an external entity client file that contains Other Entries transactions is added to a consolidated file, the transactions are brought in as Period Balances. If this external entity is converted to internal and there are internal entities with Other Entries, you will only be able to access these transactions or the Period Balances, never both.

Notes

- Internal consolidations are more suited for a consolidation made up of one legal entity with divisions, departments, funds, etc. and not a group of companies.

- If externally maintained client files are included in the entity structure, they must be physically in the file path you specified each time you re-consolidate.

- External consolidations are more suited for a group of companies, each requiring a separate engagement.

- Internal and external consolidations are compatible with SmartSync, even in synchronized child files. However, making changes to the consolidation structure or running a reconsolidation requires an online connection to the parent file.

Examples

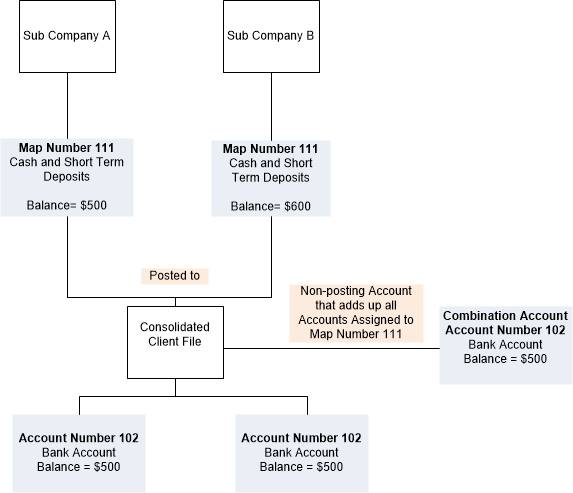

The following is an example of a consolidated file containing two sub-companies. This example is unchanged whether the sub companies' records are maintained internally or in external client files.

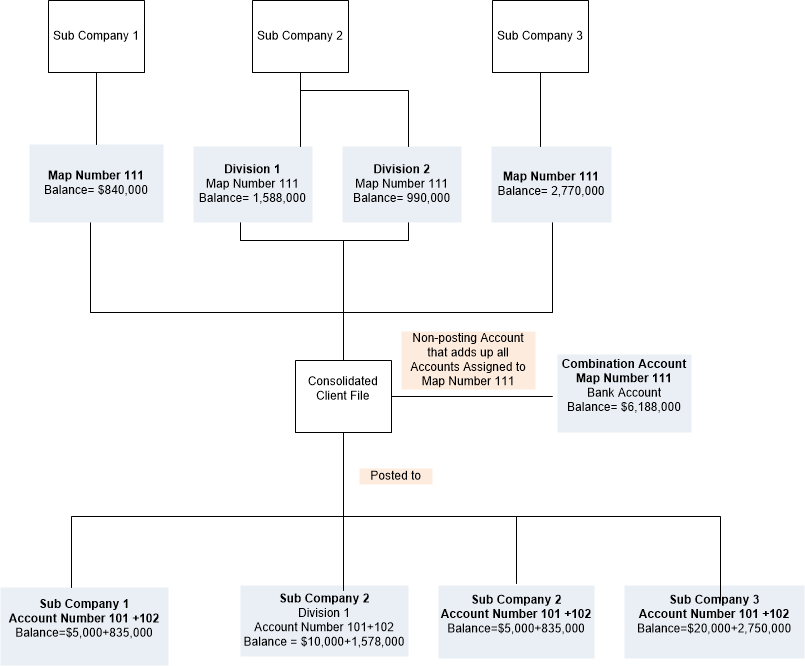

The following is an example of a consolidated corporation containing sub companies and divisions. This example is unchanged whether the sub companies' records are maintained internally or in external client files.