Completing the detailed audit response area

To complete the Detailed Audit Response area:

-

-

Determine the Assessed risks at assertion level and whether the assessed risks have changed from the previous period. This section is automatically populated from the Financial Statement Areas worksheet, RMM column.

-

Using professional judgment, determine the appropriate nature and extent (mix) of audit procedures to address each assertion. If your firm has elected to include the audit response columns in the Financial Statement Areas worksheet, this section is automatically populated from the worksheet instead of manually in the work program document. The types of suggested audit procedures include:

-

Substantive procedures - basic are typical procedures performed on most audits. These procedures should always be tailored to address the assessed risks with any unnecessary procedures removed. Where the risk of material misstatement is very low, no further procedures may be required.

-

Substantive procedures - extended are procedures performed in situations where the assessed risks for an assertion are higher than what would be covered by basic procedures, where specific or significant risks exist. These procedures also include tests of detail using sampling techniques.

-

Substantive analytical procedures can be used where an amount can be predicted and then compared to actual amounts.

-

Tests of controls are used to evaluate the operating effectiveness of controls at the assertion level. Depending on the extent of testing, tests of control may reduce risk from a high level to moderate or even low levels.

-

Audit procedures that address multiple assertions may eliminate or reduce some other tests.

-

Perform tests of controls over comparable test of details. Sample sizes are generally smaller.

-

Work performed (such as tests of controls) on other parts of the transaction stream.

-

Using professional judgment, determine whether the outlined procedures are sufficient to address assessed risk.

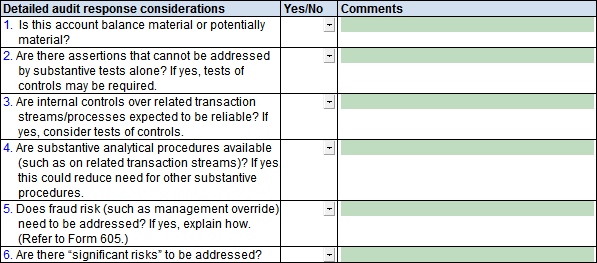

Points to consider:

This online help system applies to all CaseWare Audit, Review and Compilation products. Not all features are available in all products.

![]()

Visit us: www.caseware.com | Follow us:

© 2021 CaseWare International Inc. | Privacy | Terms of Use | Trademarks